The Scoreboard at Halftime

Six months in, here’s where the portfolio stands against the major indexes—and what changed in June.

It’s just after 5:00 a.m. in Port of Spain, and the courtyard is unusually cool this morning. Coffee number one is doing its job while the dogs are somewhere out in the yard conducting their daily investigation. No barking yet, which usually means they’ve found something worth examining. While they worked their beat, I ran through the portfolio numbers. With the first half of the year now behind us, it seemed like a good time to step back from the day-to-day market noise and see exactly where the portfolio stands relative to the major indexes.

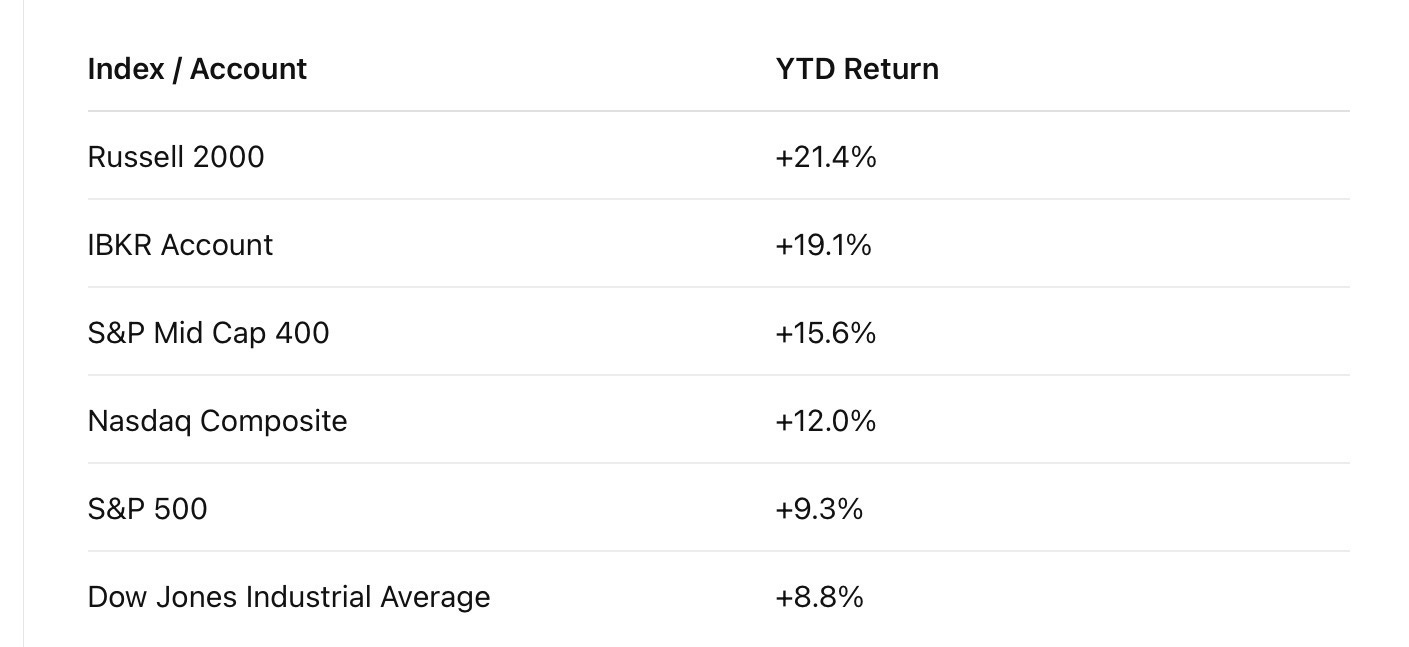

I pulled the IBKR performance report this morning, and the account is currently up +19.09% year to date on a time-weighted return basis.

That matters because TWR is the cleaner comparison number. It adjusts for deposits and withdrawals, which makes it a better way to compare the portfolio against major indexes.

Here is where things stand:

The account is still ahead of the S&P 500, Nasdaq, Dow, and Mid Caps. The only major benchmark currently ahead is the Russell 2000, which is actually a fair comparison because this portfolio has behaved much more like a high-beta small/mid-cap growth and rotation account than a plain index portfolio.

The honest read is this:

The year is still strong, but the last few weeks changed the shape of the performance.

Before the June pullback, the account had been well above +30% YTD. By the end of June, that had already cooled to roughly +21.7%. After the semi, memory, and ARM-related volatility, the account is now closer to +19.1%.

That is not a broken portfolio.

That is a portfolio that stopped running laps around the market for a few days and is now breathing like a normal human instead of a caffeinated greyhound.

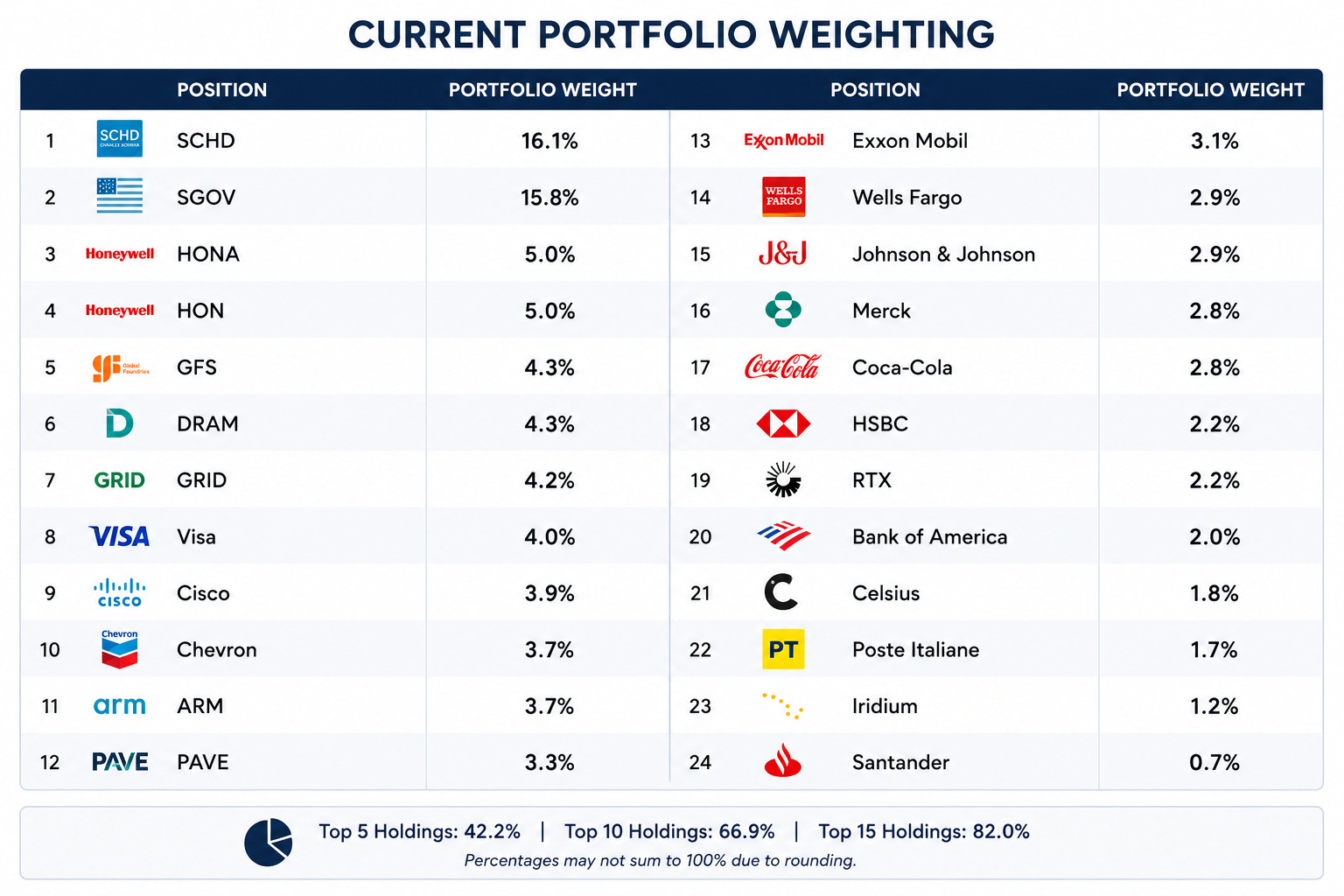

At the sector level, the account is still built around a barbell: broad dividend exposure and short-duration Treasury exposure on one side, with technology, industrials, energy, financials, and healthcare on the other.

The main drag recently has come from the higher-volatility growth sleeve, especially semiconductors and memory. The stabilizer has been the structure around SCHD, SGOV, defensives, financials, and industrials.

So the conclusion is simple:

The account is no longer in runaway outperformance mode.

But it is still ahead of most major indexes, still structured, and still very much in the game.