The Pressure Shifted: Oil Is Falling, But Markets Are Selling Anyway

For weeks energy was the problem…. This morning, oil is falling and stocks are still under pressure — which tells you rates and liquidity have moved back to center stage.

The overnight tone deteriorated meaningfully.

The biggest change is not oil. In fact, oil is helping. WTI has fallen below $90 and Brent is near $91, removing one of the largest inflation and tightening pressures that defined much of May. Yet equity futures are lower across the board, the VIX has pushed back above 20, and Treasury yields remain pinned near 4.54%.

That shift matters. The market is no longer fighting an energy shock. Instead, it is confronting restrictive financial conditions directly. Rising yields, a firm dollar, and USDJPY above 160 are doing more of the heavy lifting. The good news is that credit remains calm. LQD and HYG continue to behave normally, suggesting the system is under pressure but not under stress. For now, this remains a correction and rotation environment rather than a liquidity event.

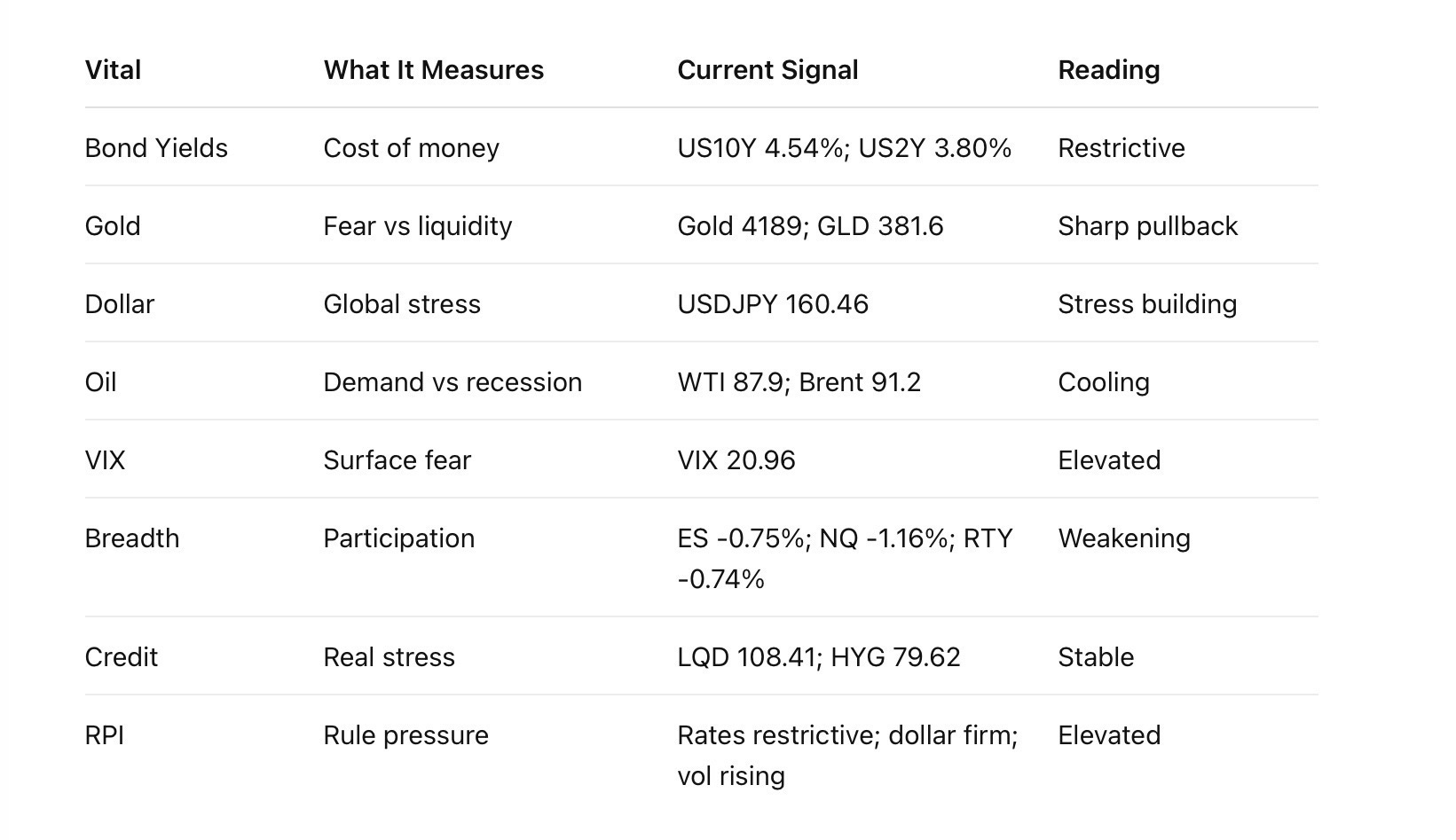

🛡 IRON VITALS — Wednesday 10 Jun 2026 — 6:15 AM AST

Market Temperature:

TESTING

Rule Pressure Index (RPI):

ELEVATED

⸻

⸻

What This Means

The overnight tone weakened materially.

The biggest change is not oil.

The biggest change is rates remaining elevated while volatility pushes back above 20 and equity futures sell off broadly.

Pressure points:

10Y yield remains near 4.54%

USDJPY above 160

VIX above 20

Nasdaq futures down more than 1%

The offset remains energy.

WTI has fallen below 90 and Brent is near 91, removing one of the largest inflation and tightening pressures from the system.

Credit remains orderly, which is preventing a routine risk-off session from becoming something larger.

This morning’s message:

Financial conditions remain restrictive, but energy pressure is easing faster than risk appetite.

⸻

⚓ ANCHOR VITALS — Wednesday 10 Jun 2026 — 6:15 AM AST

1️⃣ Equities Structure

• SPX ~7387

• NDX ~29085

• RUT ~2867

Read: Weakening. Broad overnight selling led by technology.

⸻

2️⃣ Rates Complex

• US10Y ~4.54%

• US2Y ~3.80%

• TLT ~85.07

Read: Restrictive. Rates remain the dominant macro headwind.

⸻

3️⃣ Credit

• LQD 108.41

• HYG 79.62

Read: Calm. No evidence of funding stress.

⸻

4️⃣ FX Complex

• USDJPY 160.46

• EURUSD 1.1556

• USDCNH 6.78

Read: Dollar pressure building. Yen weakness remains a concern.

⸻

5️⃣ Volatility

• VIX 20.96

Read: Elevated. Above the comfort zone but below stress-event levels.

⸻

6️⃣ Commodities

• WTI 87.94

• Brent 91.21

• Gold 4189

• Silver 64.07

• Copper 6.24

Read: Energy cooling. Precious metals and industrial metals under pressure.

⸻

ANCHOR STATUS

TESTING

Short Read

Anchor is holding because the system’s shock absorbers are still functioning:

Credit stable

Oil falling

No liquidity stress

But pressure is increasing from:

Rising yields

VIX above 20

USDJPY above 160

Weakening equity futures

The market is not broken.

It is absorbing pressure.

The next major test is whether credit remains calm while yields stay above 4.5%. If credit holds, this remains a correction and rotation environment rather than a systemic stress event.