The Market Passed the Test. The Pressure Never Left.

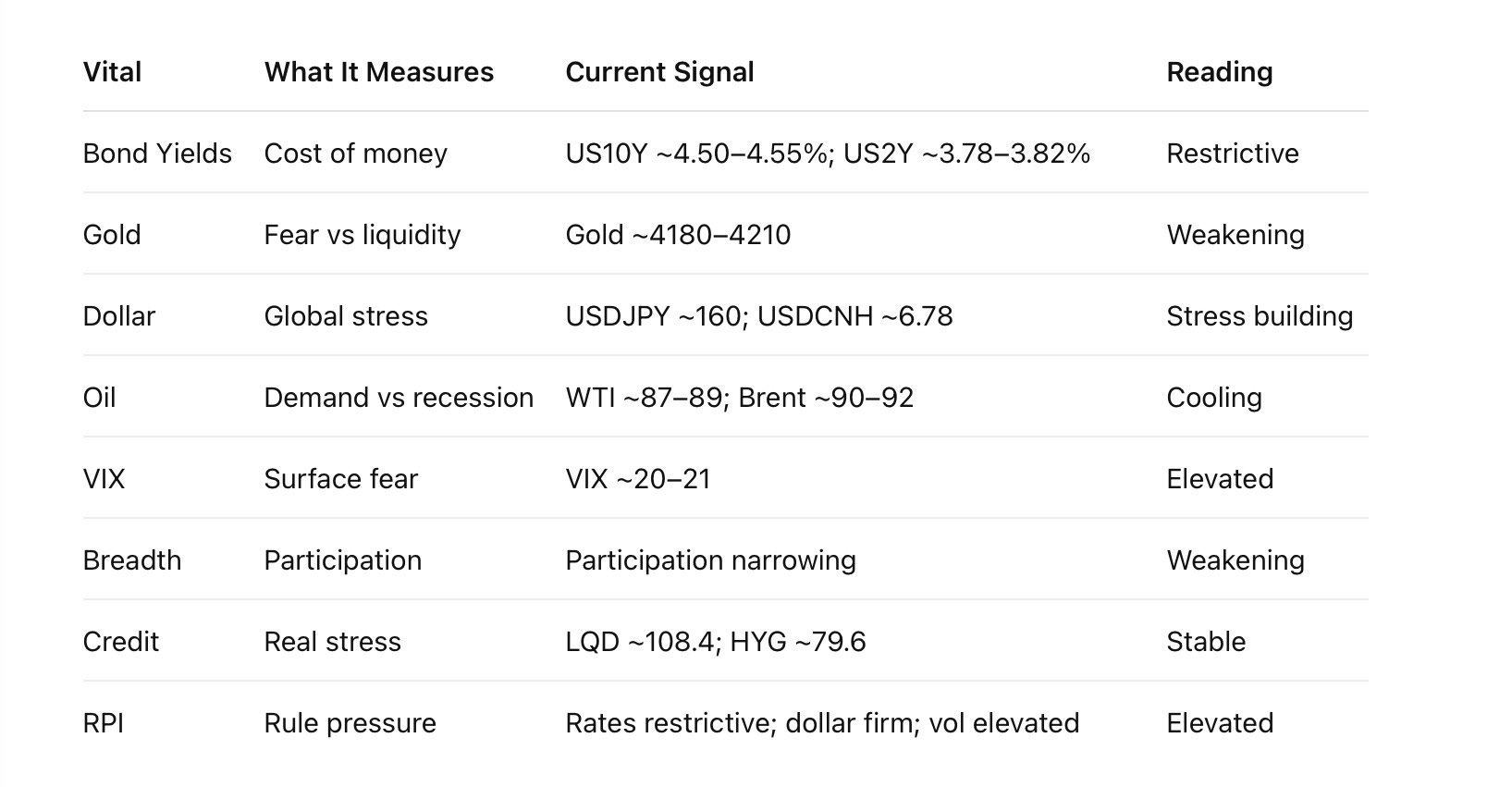

Yields stayed above 4.5%. Volatility stayed above 20. The dollar stayed firm. Yet credit remained stable and the system kept functioning.

The week ends with a market that continues to absorb pressure better than many expected.

The pressure stack remains intact. Treasury yields are still elevated, USDJPY remains above 160, and volatility is holding above its recent comfort zone. Under normal circumstances, that combination would create far more damage beneath the surface than we are currently seeing.

The difference is credit. Credit markets remain calm, funding conditions remain orderly, and there is still no evidence of forced liquidation. At the same time, oil has continued moving in the right direction. WTI below $90 and Brent near $91 represent a dramatically different backdrop from the triple-digit crude environment that dominated earlier in the cycle.

The result is a market caught between two realities. Commodity pressure is easing, but financial conditions remain restrictive. That leaves the regime neither fully risk-on nor risk-off. Leadership remains selective, participation remains narrow, and the system remains stable—but still under pressure.

🛡 IRON VITALS — Friday 12 Jun 2026 — 5:40 AM AST

Market Temperature:

TESTING

Rule Pressure Index (RPI):

ELEVATED

⸻

⸻

What This Means

The week closes with a market that remains remarkably resilient despite restrictive conditions.

The pressure stack is still present:

Treasury yields remain elevated

USDJPY remains above 160

Volatility remains above its comfort zone

Yet the system continues to absorb that pressure.

The reason is simple:

Credit has not cracked.

Meanwhile, oil continues to move in the opposite direction of the major macro risks. WTI below 90 and Brent near 91 are materially different from the triple-digit crude environment that dominated earlier in the cycle.

That leaves the market in an unusual position:

Financial conditions remain restrictive while commodity pressure is easing.

The result is a regime that is neither fully risk-on nor risk-off.

It remains a market driven by selective leadership rather than broad participation.

⸻

⚓ ANCHOR VITALS — Friday 12 Jun 2026 — 5:40 AM AST

1️⃣ Equities Structure

• SPX ~7380–7420

• NDX ~28850–29150

• RUT ~2840–2870

Read: Testing. Leadership remains concentrated.

⸻

2️⃣ Rates Complex

• US10Y ~4.5%+

• US2Y ~3.8%

• TLT ~85 area

Read: Restrictive. Still the primary headwind.

⸻

3️⃣ Credit

• LQD ~108.4

• HYG ~79.6

Read: Stable. No funding stress visible.

⸻

4️⃣ FX Complex

• USDJPY ~160

• EURUSD ~1.15

• USDCNH ~6.78

Read: Dollar pressure elevated.

⸻

5️⃣ Volatility

• VIX ~20–21

Read: Elevated but controlled.

⸻

6️⃣ Commodities

• WTI ~88

• Brent ~91

• Gold ~4190

• Silver ~64

• Copper ~6.2

Read: Energy cooling; metals soft.

⸻

ANCHOR STATUS

TESTING

Short Read

The week’s message is straightforward:

Oil is no longer the problem.

Rates are.

As long as credit remains stable and oil remains contained, the market can continue functioning despite restrictive financial conditions.

The risk is not what oil is doing.

The risk is whether elevated yields eventually begin transmitting stress into credit and broader participation.

For now:

ANCHOR remains TESTING.

IRON remains ELEVATED.