The Market Chose Megawatts Over Missiles Today

Markets have a way of revealing what they actually care about once the noise fades. Today was one of those sessions.

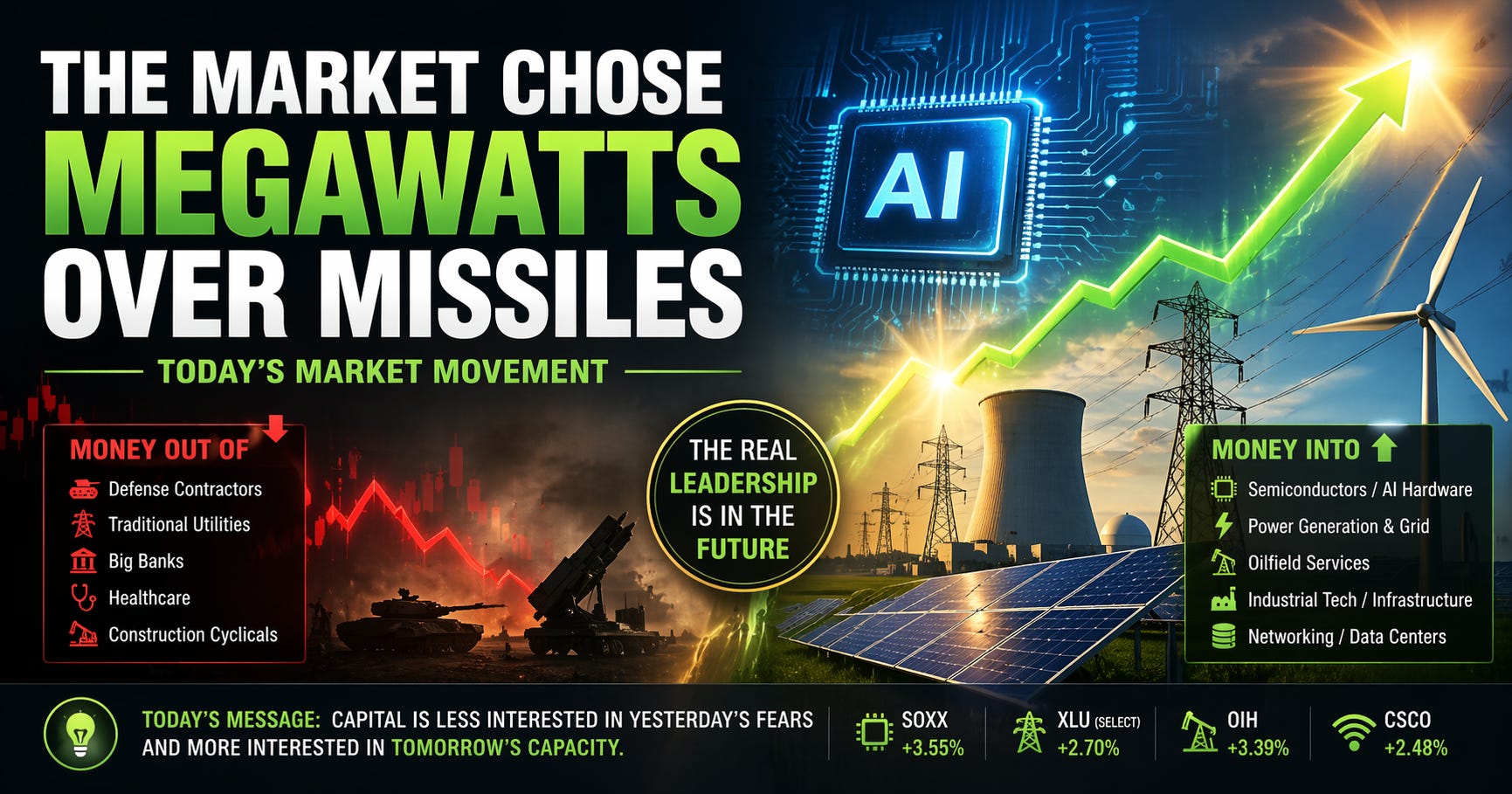

For weeks, much of the conversation has centered around geopolitics, defense spending, oil headlines, and the usual catalog of macro anxieties. Yet when capital had to choose where to go today, it made a very clear decision: money rotated toward growth infrastructure, power demand, and AI buildout—and away from many of the sectors that had previously benefited from fear.

That distinction matters.

Semiconductors led aggressively. Not just the obvious mega-cap names, but the broader complex. AI hardware, networking, foundry exposure, and second-tier chip names all participated. That is usually a stronger signal than one or two household names carrying an index. It suggests investors were not simply buying a headline—they were buying the ecosystem.

The next layer was even more interesting.

Power generation, grid exposure, and industrial names tied to electricity demand also saw meaningful strength. This is the part of the story many still underestimate. The AI trade is no longer just about chips. Chips need servers. Servers need cooling. Cooling needs power. Power needs transmission, transformers, utilities, and physical infrastructure. The market increasingly understands that the real winners may not only be the companies building intelligence, but also those supplying the energy required to run it.

In plain English: the market is starting to price the picks, shovels, and power plants behind the narrative.

At the same time, several “safety” areas struggled. Traditional defense contractors were broadly weak. Healthcare saw pressure. Large banks were soft. Even some old-line industrial cyclicals lagged. That doesn’t necessarily mean those sectors are broken, but it does suggest capital was looking forward rather than hiding.

This was not a classic defensive session. It was a selective offensive one.

There was also nuance inside energy. Oil producers were mixed, while oilfield service names showed better relative strength. That can imply investors prefer activity and cash flow tied to production demand rather than pure commodity price speculation. Again, the pattern was practical over theoretical.

The deeper message from today’s tape is that leadership may be changing shape.

For much of the past cycle, market leadership often came from a narrow group of technology giants or from fear-driven trades tied to uncertainty. Today looked different. Breadth within semis improved. Infrastructure-linked names participated. Utility exposure worked only where growth demand exists. That is a more complex, and arguably healthier, kind of participation.

Of course, one day does not make a new regime. Markets love to fake breakouts and stage one-session rotations that disappear by next week. Confirmation always matters more than excitement. If these same groups continue leading into next week—semis, power, networking, selective industrial tech—then today may prove to be more than noise.

If they reverse immediately, then this was simply another squeeze in an impatient market.

But if today was the opening chapter of a larger move, the message was simple:

Capital is less interested in yesterday’s fears and more interested in tomorrow’s capacity.

Less missiles. More megawatts.

And that is worth paying attention to.