The First Bell After the Holiday

Wall Street returns from the July 4th break with optimism, but the market’s internal map remains remarkably selective.

It’s 8:00 AM in Trinidad. A steady rain has settled in after a long night watching a weather-delayed England–Mexico World Cup match. I managed a couple of hours of sleep before discovering the dogs had apparently conducted another overnight search operation through the living room. After restoring some semblance of order, coffee number one is finally in hand and Iron Bank is open.

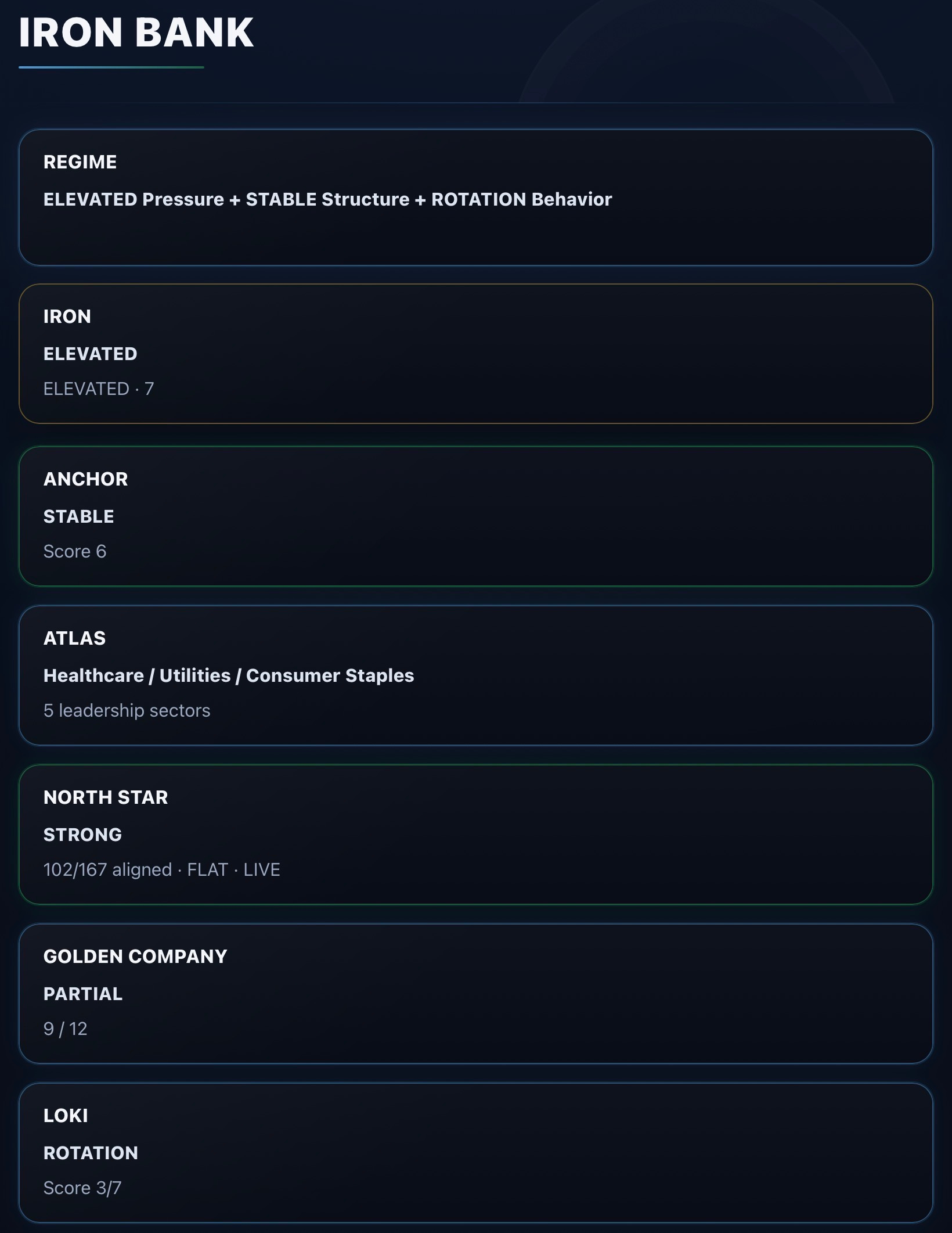

After a three-day holiday weekend, the first thing traders will notice is that futures are pointing higher. But beneath the surface, Iron Bank is telling a much more measured story.

The overall regime remains Elevated Pressure with Stable Structure and Rotation Behavior.

In other words, this isn’t a market that’s broken, nor is it one firing on all cylinders. It’s a market still climbing while working against macro headwinds.

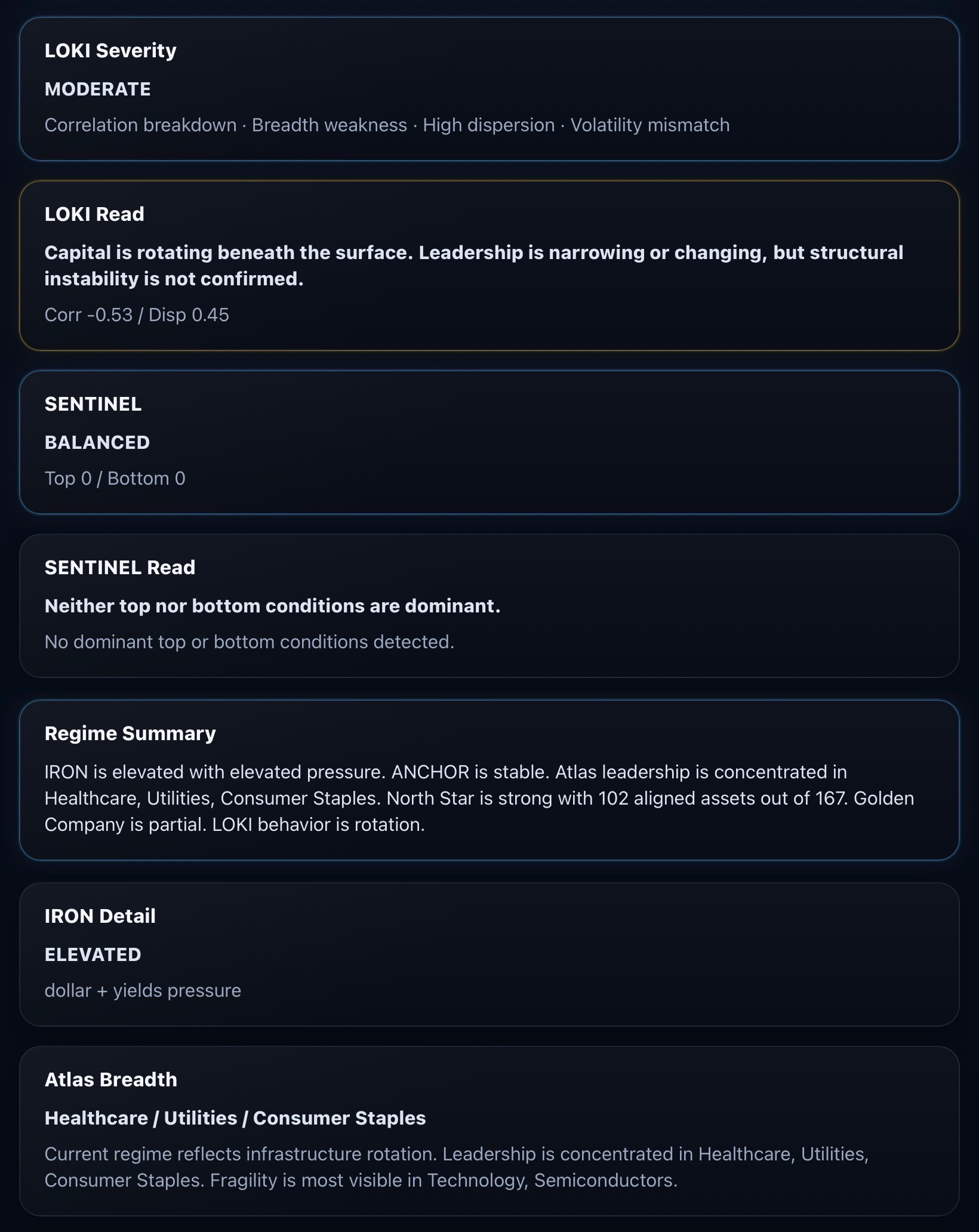

The IRON reading remains elevated, reflecting continued pressure from higher interest rates and a strong U.S. dollar. Neither has eased enough to remove the friction that’s been building beneath the surface over recent months.

At the same time, ANCHOR remains stable. Credit markets continue functioning normally, liquidity remains intact, and there are still no signs that systemic stress is spreading through financial markets. Elevated pressure is something to respect, but it hasn’t become instability.

Participation also remains encouraging. North Star shows 102 of 167 assets aligned, or just over 61% of the market. That’s consistent with a market that’s still trending higher, even if leadership has narrowed.

That narrowing is exactly what LOKI continues to detect.

LOKI remains in Rotation with moderate severity. Correlations remain low while dispersion stays elevated, indicating capital is moving between sectors rather than exiting equities altogether.

That’s an important distinction.

Rotation creates new leaders.

Liquidation creates broad losers.

Iron Bank says we’re still in the first environment.

The biggest surprise this morning is where that leadership actually sits.

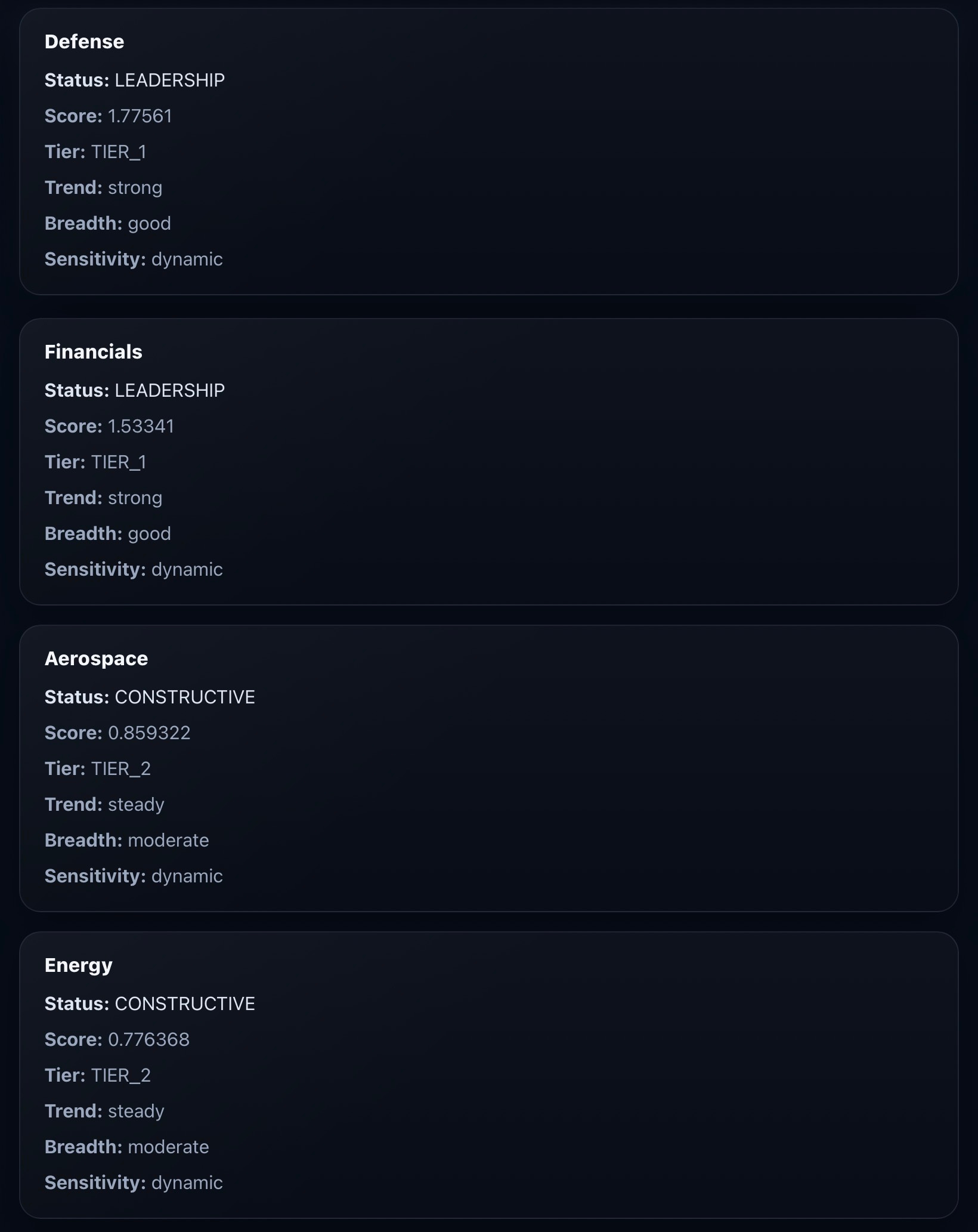

According to ATLAS, leadership remains concentrated in Healthcare, Utilities, Consumer Staples, Materials, Defense, and Financials. These are sectors that continue attracting institutional capital despite the higher index futures.

Meanwhile, Technology and Semiconductors remain classified as Breaking. That doesn’t necessarily mean they cannot rally today after the long weekend. It means the broader participation required to restore durable leadership has not yet appeared.

For investors, Golden Company continues to deliver the same message it has for several weeks: Partial Deployment.

This isn’t an environment for hiding in cash.

It also isn’t an environment for buying everything that’s moving.

It’s an environment that rewards patience, discipline, and selective exposure to sectors where leadership has already been confirmed.

The opening session after a long holiday weekend often produces strong moves as traders reposition portfolios and react to several days of accumulated news. The question isn’t whether the indexes open higher or lower.

The more important question is whether today’s buying broadens participation across the market or simply rotates money into another group of stocks.

For now, Iron Bank continues to describe a market that remains healthy enough to participate in, but selective enough that where you invest still matters more than simply being invested.