Morning Briefing — The Pressure Is Easing. The Market Still Isn’t Broadening Out.

Energy is no longer the problem, participation is…

The regime heads into Friday morning in a much healthier position than it was just a few weeks ago.

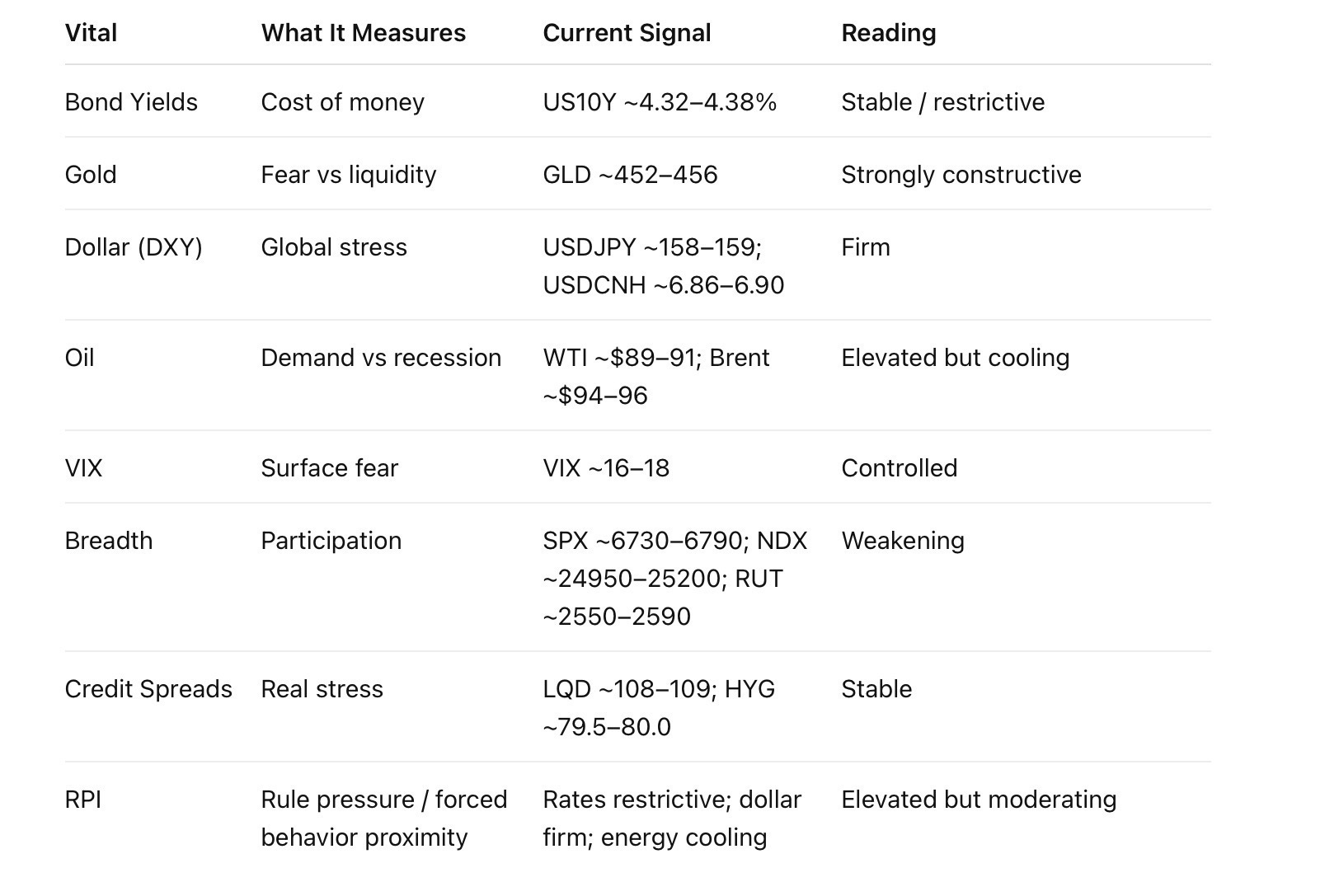

The energy shock that dominated May has faded, with crude holding below the levels that were driving tightening concerns across the system. Rates remain restrictive and the dollar remains firm, but neither is accelerating. Credit remains orderly, volatility remains contained, and there is still no sign of forced behavior beneath the surface.

The remaining issue is participation. Indexes continue to look stronger than many of the stocks underneath them, suggesting leadership remains concentrated rather than broad. Translation: conditions have improved significantly, but this still looks more like stabilization than expansion. Pressure is easing. The system is functioning. The next step is seeing whether participation finally starts to catch up.

Rates and the dollar remain the primary constraints on risk-taking, but both have settled into a steady state rather than becoming a fresh source of tightening. Meanwhile, oil’s retreat into the low-90s has removed one of the largest pressure points from the regime map. Gold remains near highs, suggesting investors still value protection even as market stress indicators remain calm.

The regime remains constructive for selective leadership, but broad participation continues to lag. The system is intact. Conditions are improving. The missing piece is confirmation from the rest of the market.

🛡 IRON VITALS — Friday 5 Jun 2026 — 5:40 AM AST

Market Temperature:

WARM (restrictive, but stable)

Rule Pressure Index (RPI):

ELEVATED (rates + dollar pressure; energy moderated)

⸻

⸻

What This Means

The week is ending in a far healthier position than where it began.

The energy shock that dominated May has largely faded from the primary risk list, with crude remaining below the stress zone that previously drove tightening concerns.

Rates remain restrictive and the dollar remains firm, but neither is accelerating.

Gold continues to hold near highs, suggesting capital remains interested in protection even while market stress indicators stay calm.

The stabilizers remain intact:

* Credit orderly

* Volatility contained

* No forced behavior visible

The one issue still lingering is participation.

Indexes continue looking healthier than many of the stocks underneath them.

Translation: conditions have improved significantly, but this still looks like stabilization rather than full expansion.

The pressure is easing.

The system has not completely normalized.

⸻

⚓ ANCHOR VITALS

Friday 5 Jun 2026 — 5:40 AM AST

(Context: Pre-US Open)

⸻

1️⃣ Equities Structure

• SPX ~6730–6790

• NDX ~24950–25200

• RUT ~2550–2590

Short read: Stable. Participation remains selective.

⸻

2️⃣ Rates Complex

• TNX ~4.32–4.38

• TLT ~84–85

• SHY ~82.1–82.3

Read: Restrictive but orderly.

⸻

3️⃣ Credit

• LQD ~108–109

• HYG ~79.5–80.0

Read: Calm. Funding stress absent.

⸻

4️⃣ FX Complex

• USDJPY ~158–159

• USDCNH ~6.86–6.90

• USDCHF ~0.79–0.80

Read: Dollar firm, orderly.

⸻

5️⃣ Volatility

• VIX ~16–18

Read: Controlled.

⸻

ANCHOR STATUS:

INTACT