Energy and Rates Tighten the System Again : Morning Regime Note — March 16 3:30am AST

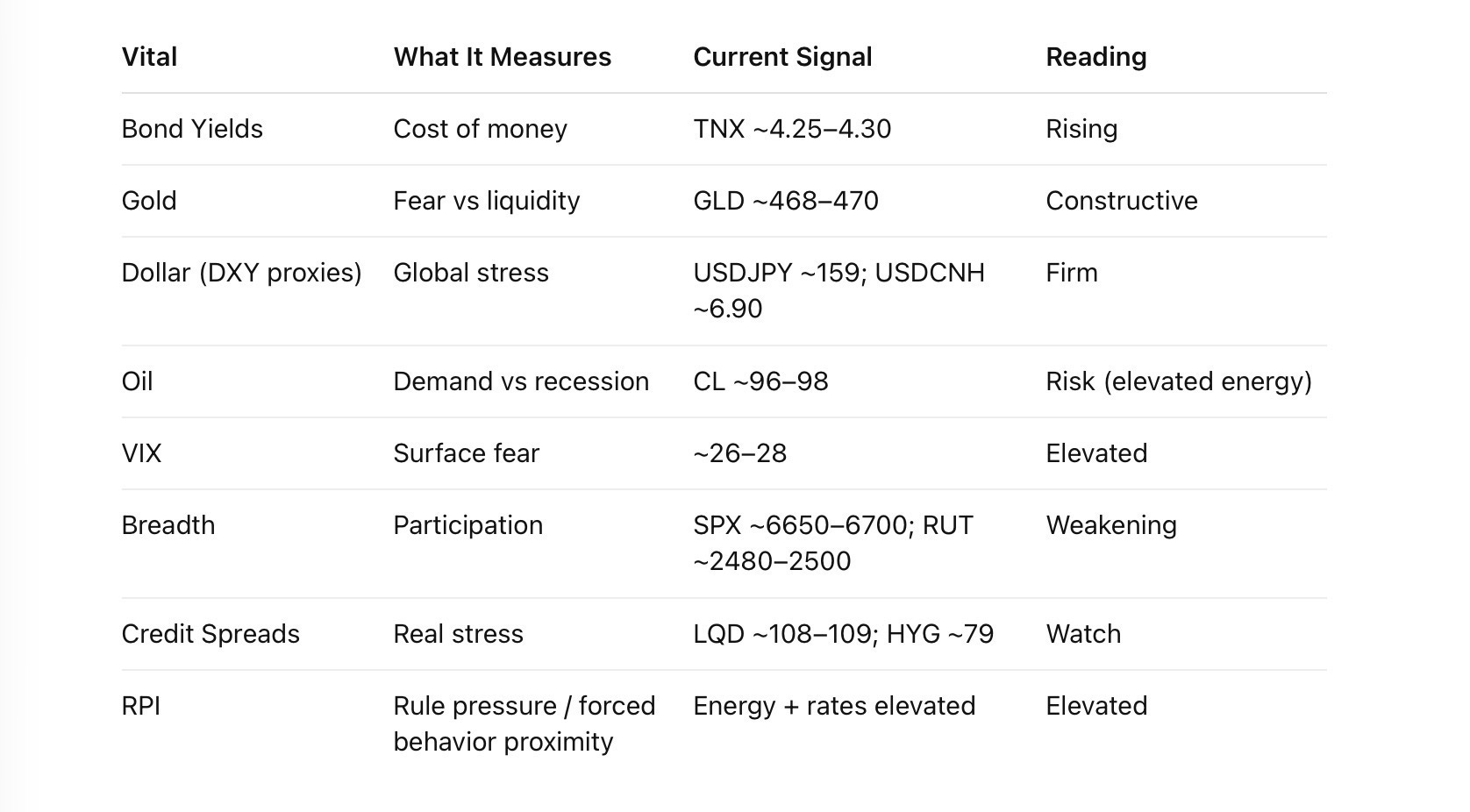

Markets begin the week under persistent cost pressure from both energy and rates. Crude remains elevated near $96–98, the 10-year yield is holding around ~4.25–4.30%, and volatility remains in the mid-to-high 20s. Equities are trading weaker with small caps lagging, while credit markets remain functional. The environment reflects tightening financial conditions rather than systemic stress.

Reader Takeaway:

Energy and rates staying elevated are keeping markets under pressure, but stable credit markets suggest the system is adjusting rather than breaking.

What Matters:

The combination of elevated oil prices and rising Treasury yields continues to tighten financial conditions. Crude holding near the high-$90s sustains inflation pressure while yields near cycle highs increase the cost of capital. Volatility remains above normal levels, reflecting elevated risk premiums. Equity participation remains narrow with defensive and commodity-linked sectors leading while small caps lag. Credit instruments such as LQD and HYG remain orderly, indicating funding markets are still functioning despite softer risk assets.

Regime Call:

Markets remain in a cost-pressure regime driven by elevated energy prices and rising yields.

Trigger:

A sustained move in crude above $100, combined with VIX expansion above ~30 and clear credit spread widening, would signal escalation toward forced-behavior conditions.

🛡 IRON VITALS — Monday 16 Mar 2026 — 3:30 AM AST (Pre-Market)

Market Temperature:

WARM — PRESSURE ELEVATED

Rule Pressure Index (RPI):

ELEVATED (energy + rates pressure)

⸻

⸻

What This Means

Energy prices remain elevated near the mid-90s, maintaining cost pressure across the system.

Rates are holding near cycle highs, which tightens financial conditions further.

Volatility remains above normal levels, indicating risk premiums are still elevated.

Equity participation is narrow with small caps lagging and leadership concentrated in defensive and commodity-linked sectors.

Credit markets remain functional, though spreads have softened slightly as risk assets adjust.

This is a high-pressure environment but not a systemic break.

Markets are adjusting to persistent cost pressure from energy and rates simultaneously.

Full Structural Diagnosis can be found at our Research Portal.

⸻

⚓ ANCHOR VITALS

Monday 16 Mar 2026 — 3:30 AM AST (Pre-Market)

⸻

1️⃣ Equities Structure

• SPX ~6680

• NDX ~24,500

• RUT ~2490

• N225 ~54,000 area

Read: Weakening but orderly.

⸻

2️⃣ Rates Complex

• TNX ~4.27

• TLT ~86–87

• SHY ~82.5

Read: Duration under pressure.

⸻

3️⃣ Credit

• LQD ~108–109

• HYG ~79

• KRE ~63

Read: Credit soft but functioning.

⸻

4️⃣ FX Complex

• USDJPY ~159

• USDCNH ~6.90

• USDCHF ~0.79

Read: Dollar firm but orderly.

⸻

5️⃣ Volatility

• VIX ~27

Read: Elevated risk premium.

⸻

ANCHOR STATUS

TESTING

⸻

Markets are entering the week with energy and rates still elevated, which keeps the system under pressure.

However, the key stabilizing factor remains credit integrity.

As long as credit markets stay functional, the environment typically remains repricing and rotation rather than systemic instability.