Beta Isn’t Risk — It’s How Risk Shows Up

Why drawdowns that look the same can signal very different kinds of risk

Right now, a lot of people are talking past each other.

The index looks fine.

Volatility is elevated but not panicked.

And yet some portfolios are down modestly, while others are down a lot.

The explanation that follows is familiar:

“That’s just high beta.”

That explanation misses the point.

Because two portfolios can be down the same amount for very different reasons — and only one of them is actually broken.

Beta Is Sensitivity, Not Fragility

Beta is often reduced to a cartoon:

High beta = volatile

Low beta = stable

In reality, beta is not risk.

It’s how risk expresses itself when conditions change.

Beta is a response function. It tells you how something moves relative to the market — not why it moves, and not whether it survives the move.

High beta can be intentional.

It can be sized.

It can be liquid.

High beta is not reckless if it is understood and reversible.

The real danger isn’t volatility.

It’s carrying beta you don’t recognize.

The Beta Most People Miss

Price beta is obvious.

Structural beta is not.

That’s where problems usually come from.

Structural beta shows up as:

Liquidity beta — exits matter more than entries

Correlation beta — diversification fails under stress

Funding or duration beta — conditions tighten suddenly

Narrative beta — crowded ideas unwind together

Here’s the key point:

The most dangerous portfolios aren’t high beta — they’re unidentified beta.

That’s how people get surprised while telling themselves they’re being patient.

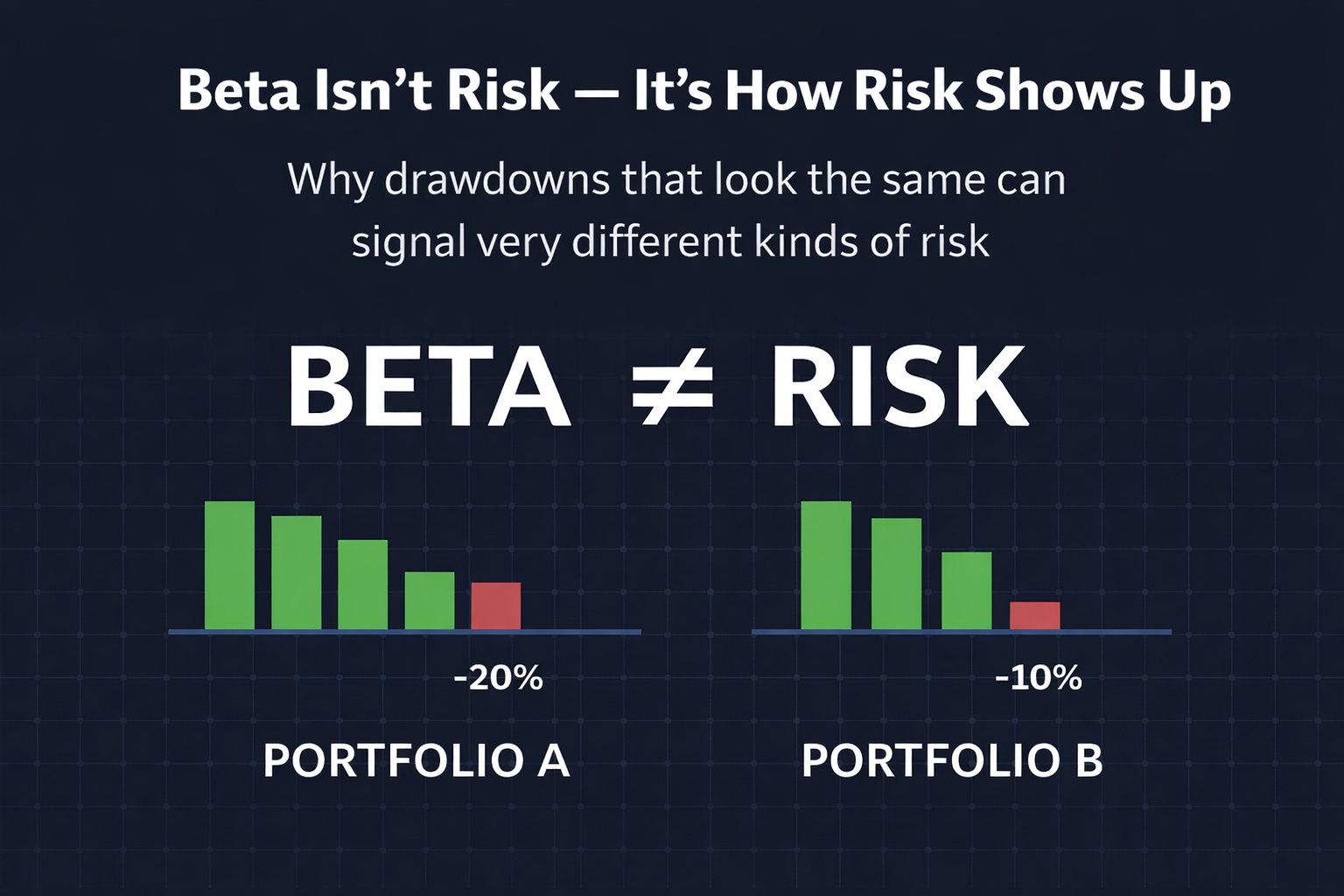

Same Drawdown, Different Risk

Consider two portfolios.

Portfolio A

Down 20%

Liquid

Multiple drivers

Loss driven by broad stress

Portfolio B

Down 10%

Illiquid

Highly correlated

Loss driven by structural unwind

On the surface, Portfolio B looks safer.

In reality, Portfolio A can adjust.

Portfolio B may not be able to move at all.

So the uncomfortable question is:

Which one is actually at risk?

Most people have been trained to answer that wrong.

About the “Relax” Argument

Yes, volatility is normal.

Yes, higher beta portfolios move more.

No, panic doesn’t help.

But calm isn’t a strategy either.

If correlations spike, beta stops behaving the way models say it should.

If liquidity disappears, conviction stops mattering.

If funding tightens, time stops being your friend.

Those aren’t emotional risks.

They’re mechanical ones.

A Simple Rule Set

This isn’t about avoiding beta.

It’s about choosing it deliberately.

A few rules that actually help:

Beta should be chosen, not discovered in a drawdown

Liquidity matters more than conviction during stress

Correlation risk appears when diversification is most trusted

Surviving matters more than being right

You can recover from volatility.

You can’t recover from being structurally trapped.

Bottom Line

Beta isn’t the enemy.

Unexamined beta is.

Two portfolios can look equally bruised while only one is fundamentally damaged. If you don’t understand the structure of your exposure, performance numbers will lie to you at exactly the wrong moment.

This isn’t about predicting the next move.

It’s about not being surprised by the one that hurts.

View the entire article here